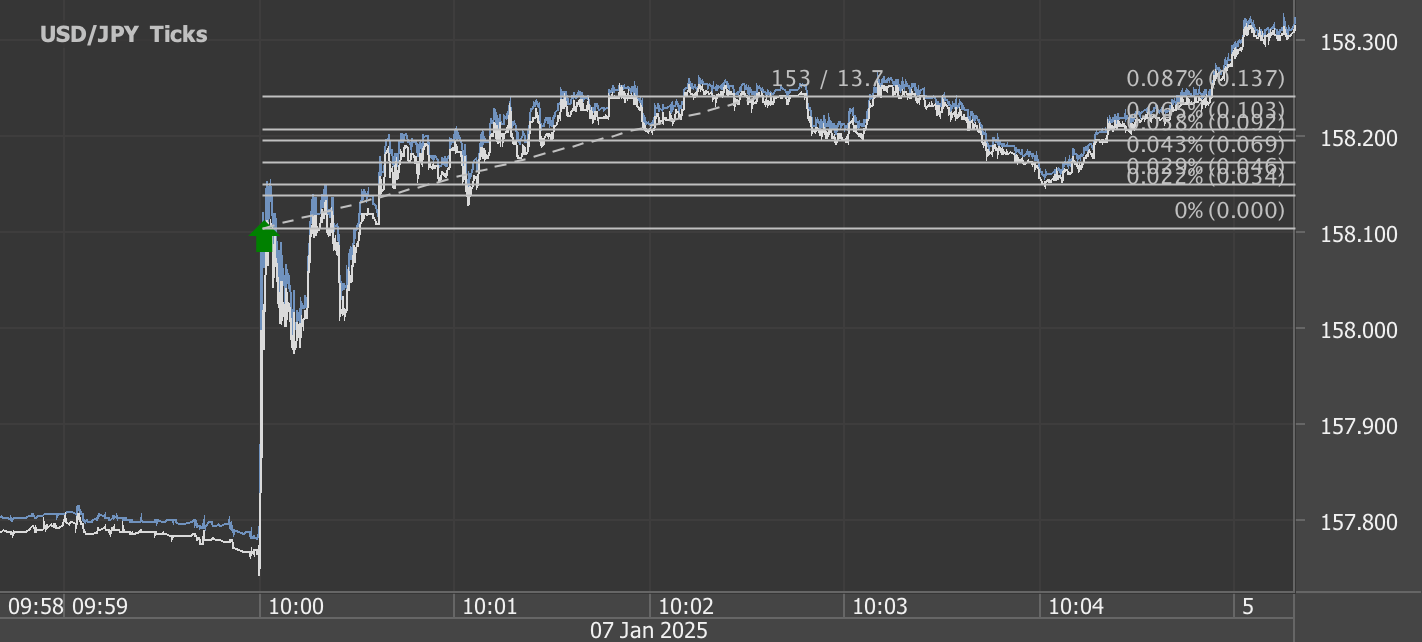

According to our analysis soybeans (ZS), corn (ZC) and wheat (WC) futures prices moved around 104 ticks (36 ticks, 40 ticks and 28 ticks) on USDA WASDE (World Agricultural Supply and Demand Estimates) and USDA Grain Stocks data on 10 January 2025.

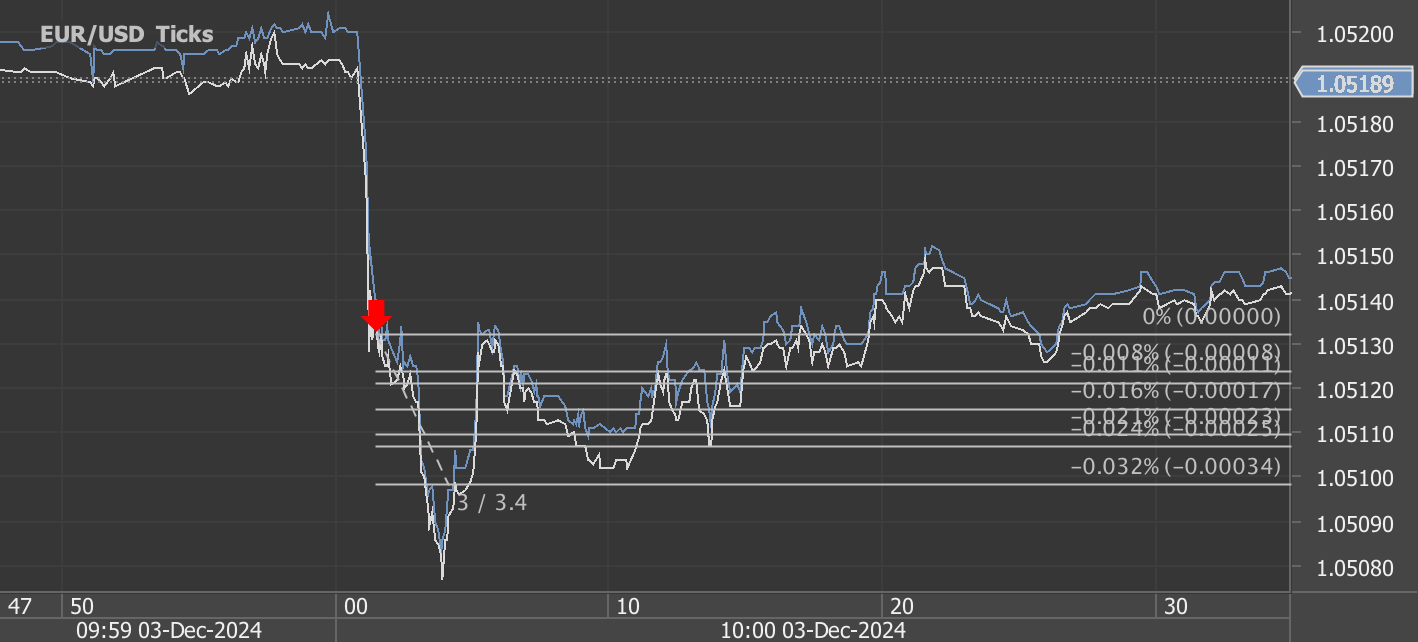

Soybeans (36 ticks)

Charts are exported from JForex (Dukascopy).

January 2025 WASDE and Grain Stocks Report: Key Takeaways for Agricultural Traders

The USDA’s World Agricultural Supply and Demand Estimates (WASDE - 656) and Grain Stocks Report released on January 10, 2025 provide a comprehensive update on the supply, demand, and stock levels for key commodities. For traders, these reports offer essential insights into potential price movements and market dynamics in the months ahead.

Below is a detailed breakdown of the key highlights for cotton, corn, soybeans, and wheat, covering both U.S. and global markets.

1. Cotton: Bearish Signals from Higher Stocks and Lower Prices

U.S. Cotton Outlook:

Production: Increased by 159,000 bales to 14.4 million bales, driven by higher yields (836 pounds/harvested acre) despite reduced harvested area in the Southwest.

Exports: Lowered by 300,000 bales to 11.0 million bales.

Ending Stocks: Increased to 4.8 million bales, pushing the stocks-to-use ratio to 38%.

Farm Price: Reduced to 65 cents per pound, reflecting ample supply and reduced export demand.

Global Cotton Market:

Production: Raised by 2 million bales to 119.4 million bales, primarily due to a 1.8 million-bale increase in China.

Consumption: Increased by 100,000 bales, driven by Bangladesh and Vietnam.

Trade: Global exports are up 225,000 bales, as gains in Brazil, Australia, and India offset the reduction in U.S. exports.

Ending Stocks: Increased by 1.9 million bales, with notable increases in China, Australia, and India.

💡 Trading Takeaway:

The cotton market presents bearish signals as higher global production and U.S. export cuts weigh on prices. Traders should monitor Southeast Asian demand closely and assess the potential impact of China’s stockpiling strategy.

2. Corn: Tighter Supplies Signal Price Support

U.S. Corn Outlook (WASDE):

Production: Cut to 14.9 billion bushels (-276 million bushels), reflecting a yield reduction to 179.3 bushels/acre (-3.8 bushels/acre).

Use:

Feed & Residual: Reduced by 50 million bushels to 5.8 billion bushels, due to lower-than-expected feed demand.

Exports: Lowered by 25 million bushels to 2.5 billion bushels.

Ending Stocks: Reduced by 198 million bushels to 1.88 billion bushels.

Farm Price: Increased to $4.25 per bushel (+$0.15), reflecting tighter supplies.

Grain Stocks Report (Corn):

Total Corn Stocks (Dec 1, 2024): 12.1 billion bushels (-1% year-over-year).

On-Farm Stocks: 7.66 billion bushels (-2%).

Off-Farm Stocks: 4.41 billion bushels (+2%).

Disappearance (Sep-Nov 2024): 4.56 billion bushels, slightly above the 4.53 billion bushels reported for the same period in 2023.

Global Corn Market:

Production: Lowered by 4.8 million tons to 1.494 billion tons, though China’s record harvest (294.9 million tons) offsets some global losses.

Trade: Global exports declined due to reductions in U.S. and Brazilian shipments.

Ending Stocks: Lowered by 3.1 million tons to 293.3 million tons, with China increasing its reserves to a record level.

💡 Trading Takeaway:

Corn prices could remain firm due to tightening U.S. supplies and strong domestic feed demand. The market will closely watch Brazil’s export pace and China’s reserve strategy as key determinants of price direction.

3. Soybeans: Higher Stocks with Strong Seasonal Demand

Grain Stocks Report (Soybeans):

Total Soybean Stocks (Dec 1, 2024): 3.10 billion bushels (+3% year-over-year).

On-Farm Stocks: 1.54 billion bushels (+6%).

Off-Farm Stocks: 1.56 billion bushels (+1%).

Disappearance (Sep-Nov 2024): 1.61 billion bushels, up 13% from the same period in 2023, reflecting stronger seasonal demand.

U.S. Soybean Outlook (WASDE):

While soybeans were not specifically highlighted in the WASDE production changes, the robust disappearance from the Grain Stocks Report signals sustained demand, especially for exports and domestic processing.

💡 Trading Takeaway:

The combination of rising stocks and strong disappearance could lead to price fluctuations. Traders should closely watch South American harvest updates and any geopolitical developments that could influence export markets.

4. Wheat: Rising Stocks Amid Strong Demand

U.S. Wheat Outlook (WASDE):

Supplies: Increased by 5 million bushels to 130 million bushels, driven by higher imports of Hard Red Spring wheat.

Domestic Use:

Feed & Residual Use: Unchanged at 120 million bushels.

Seed Use: Increased by 2 million bushels to 64 million bushels.

Exports: Steady at 850 million bushels despite by-class adjustments.

Ending Stocks: Raised by 3 million bushels to 798 million bushels (+15% year-over-year).

Farm Price: Reduced by $0.05 to $5.55 per bushel.

Grain Stocks Report (Wheat):

Total Wheat Stocks (Dec 1, 2024): 1.57 billion bushels (+10% year-over-year).

On-Farm Stocks: 467 million bushels (+16%).

Off-Farm Stocks: 1.10 billion bushels (+8%).

Disappearance (Sep-Nov 2024): 423 million bushels, up 22% from the same period in 2023, reflecting robust demand.

Global Wheat Market:

Supplies: Raised by 0.4 million tons to 1,060.7 million tons, with gains in Syria and Pakistan offsetting reductions in Uruguay.

Consumption: Lowered by 0.6 million tons, with Turkey’s demand decrease partially offset by increased usage in Ukraine.

Trade: Global exports are down 1.7 million tons due to reduced shipments from Russia and Ukraine.

Ending Stocks: Increased by 0.9 million tons to 258.8 million tons, with increases in Russia, Brazil, and Ukraine offsetting declines in China and Indonesia.

💡 Trading Takeaway:

The wheat market remains mixed. While U.S. imports and global stocks are rising, strong domestic demand and geopolitical tensions in the Black Sea region could continue to influence prices. Traders should watch for export developments and changes in demand from key buyers like Turkey and China.

Key Summary for Traders:

| Commodity | U.S. Supply Trend | Global Supply Trend | Market Sentiment |

|---|---|---|---|

| Cotton | Higher stocks | Rising global production | Bearish |

| Corn | Lower production | Slight stock decline | Bullish |

| Soybeans | Higher stocks | Strong demand | Mixed |

| Wheat | Increased imports | Higher global stocks | Mixed |

Final Thoughts:

Agricultural markets are bracing for potential price volatility as the WASDE and Grain Stocks reports highlight key supply and demand shifts. Key areas to watch include:

Cotton: Price pressure remains due to higher global production and reduced U.S. exports.

Corn: Tighter U.S. supplies and robust feed demand could support prices.

Soybeans: Despite higher stocks, strong seasonal demand may limit bearish movements.

Wheat: Strong demand contrasts with rising stocks, creating a mixed outlook sensitive to geopolitical risks.

Traders should remain alert to any new developments, particularly weather conditions in South America, policy changes in China, and ongoing geopolitical tensions, as these could significantly impact commodity prices in the coming months.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Source: https://www.usda.gov/oce/commodity/wasde/wasde0125.pdf, https://downloads.usda.library.cornell.edu/usda-esmis/files/xg94hp534/5d86qt759/xp68nc84m/grst0125.pdf

Haawks G4A is one of the fastest machine-readable data feeds for USDA data. We are beating big names in the industry by seconds. Coverage includes monthly USDA WASDE (World Agricultural Supply and Demand Estimates), quarterly USDA Grain Stocks and yearly USDA Prospective Plantings and USDA Acreage.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.