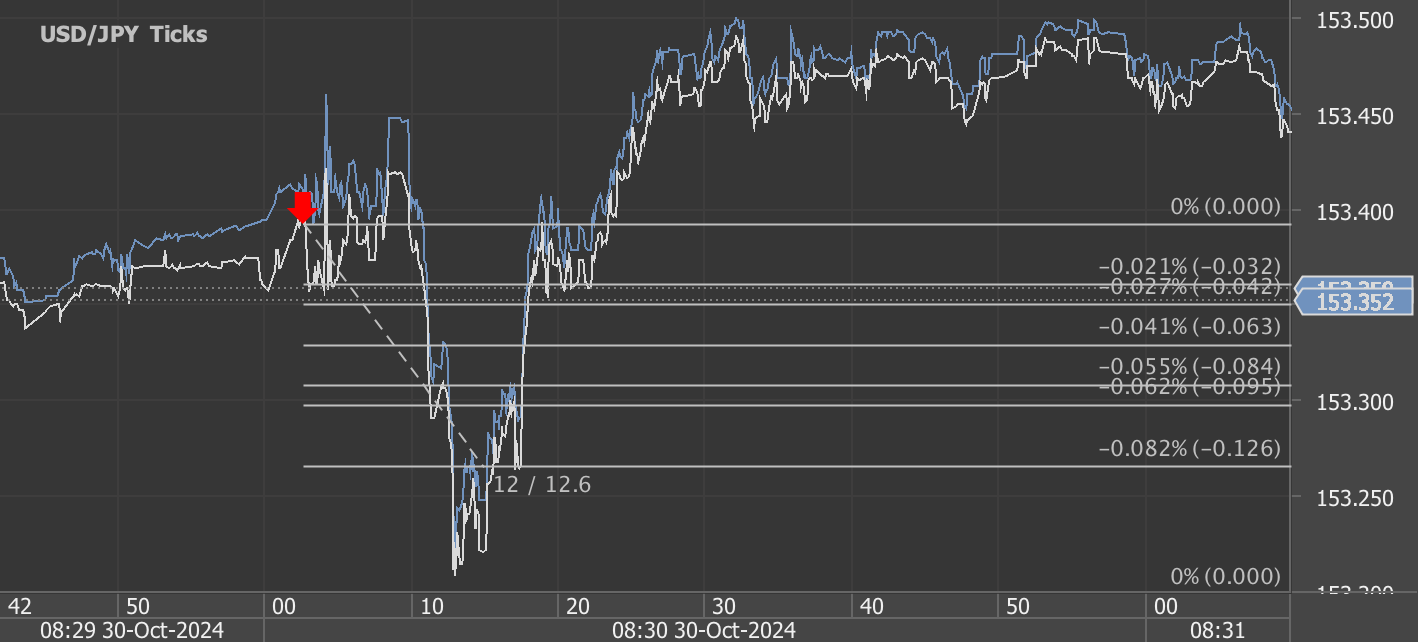

According to our analysis USDJPY and EURUSD moved 31 pips on US BLS Producer Price Index (PPI) data on 14 November 2024.

USDJPY (20 pips)

EURUSD (11 pips)

Charts are exported from JForex (Dukascopy).

October 2024 Producer Price Index Report: Key Takeaways and Insights

The U.S. Bureau of Labor Statistics (BLS) recently released its Producer Price Index (PPI) report for October 2024, highlighting an incremental rise in wholesale prices across several categories. The report provides a valuable gauge of inflation trends within the economy as it captures the price changes from producers' perspectives. Let’s dive into the major insights and explore what they mean for businesses, policymakers, and consumers.

Overview of the October PPI Data

The PPI for final demand rose by 0.2% in October, following a modest increase of 0.1% in September. Over the past 12 months, the final demand index rose by 2.4%, signaling steady, though contained, inflationary pressures on the production side. Excluding the more volatile food, energy, and trade services, the index increased by 0.3% in October and 3.5% year-over-year, indicating some underlying inflation in core producer prices.

Final Demand Services: Primary Driver of October's Price Increase

A significant portion of the October PPI increase stemmed from final demand services, which advanced by 0.3%. This rise marks a steady increase from previous months and reflects broad-based price gains within service sectors:

Services excluding trade, transportation, and warehousing showed a 0.3% increase, leading the rise in service prices.

Transportation and warehousing services experienced a 0.5% price hike, indicating higher operating costs within logistics networks.

Portfolio management services saw a notable 3.6% price increase, contributing significantly to the overall rise in service prices.

This uptick in service-related costs can affect businesses reliant on professional services, financial services, and logistics, potentially impacting prices downstream.

Final Demand Goods: A Modest Rise in Prices

The index for final demand goods increased slightly by 0.1% in October after consecutive declines. Notably:

Goods excluding food and energy climbed by 0.3%, suggesting steady demand for manufactured goods.

Energy prices fell by 0.3%, while food prices saw a modest decrease of 0.2%.

The standout here was the 8.4% jump in the price of carbon steel scrap, reflecting price fluctuations in raw materials that could affect various industries, including construction and manufacturing.

Intermediate Demand Insights: Processed and Unprocessed Goods Climb Higher

Intermediate demand, representing the cost of goods and services in the production process, displayed varied trends:

Processed goods for intermediate demand rose by 0.5% after two months of declines, largely due to higher prices for processed materials excluding food and energy. Year-over-year, however, processed goods have declined by 1.2%.

Unprocessed goods for intermediate demand saw a more significant jump of 4.1%, the largest since August 2022. A 9.9% increase in energy materials, particularly crude petroleum, drove this rise.

These price increases at the intermediate stage may signal cost pressures on manufacturers and suppliers, likely influencing prices for consumers and businesses in the near future.

Stages of Production Analysis

Examining the PPI by production stages provides additional insight into where price changes are occurring in the supply chain:

Stage 4 intermediate demand (goods closest to final production) rose 0.2%, with notable increases in diesel fuel and rents for office and retail properties.

Stage 3 intermediate demand climbed by 0.5%, driven by goods inputs like diesel fuel and slaughter poultry.

Stage 2 intermediate demand increased by 1.5%, with goods inputs up by 3.8% due to jumps in crude petroleum and carbon steel scrap.

Stage 1 intermediate demand showed a 0.3% rise, propelled by higher prices for airline passenger services and carbon steel scrap.

What These Trends Mean for the Economy

The steady increases in October’s PPI, particularly within services and intermediate goods, suggest that inflationary pressures are present but not severe. Here’s what this could mean for different stakeholders:

For businesses: Rising input costs, especially in services and core goods, may lead to increased expenses for production and logistics. Businesses may need to consider cost-management strategies or price adjustments to maintain margins.

For policymakers: The continued rise in core PPI components could influence monetary policy decisions. The Federal Reserve may view these trends as an indication of persistent inflation within the supply chain, potentially affecting interest rate policies.

For consumers: While direct consumer prices aren’t covered in the PPI, higher production costs can often translate into retail price increases. Consumers may notice price adjustments in areas affected by rising wholesale service costs, including travel, healthcare, and retail products.

Looking Ahead: What to Watch for in November

The next PPI release, scheduled for December 12, 2024, will reveal if these inflationary pressures persist into the year’s final quarter. Key areas to monitor include:

Service sector trends: As services remain a major factor in the overall PPI, any shifts here could influence broader price stability.

Intermediate demand for goods: Further rises in intermediate demand could signal ongoing supply chain pressures, especially if energy costs remain volatile.

In sum, October’s PPI report underscores that while inflationary pressures are present, they remain relatively contained and sector-specific. By keeping an eye on these trends, businesses and consumers can better anticipate potential price changes as the economy progresses into 2024.

Start futures forex fx news trading with Haawks G4A low latency machine-readable data, one of the fastest machine-readable news trading feed for US economic and commodity data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.