According to our analysis there was a potential of 161 pips / ticks profit out of the following 3 events in September 2024. The potential performance in 2023 was 13,607 pips / ticks.

September 2024

US BLS Job Openings and Labor Turnover Survey (JOLT) (72 pips / 4 September 2024)

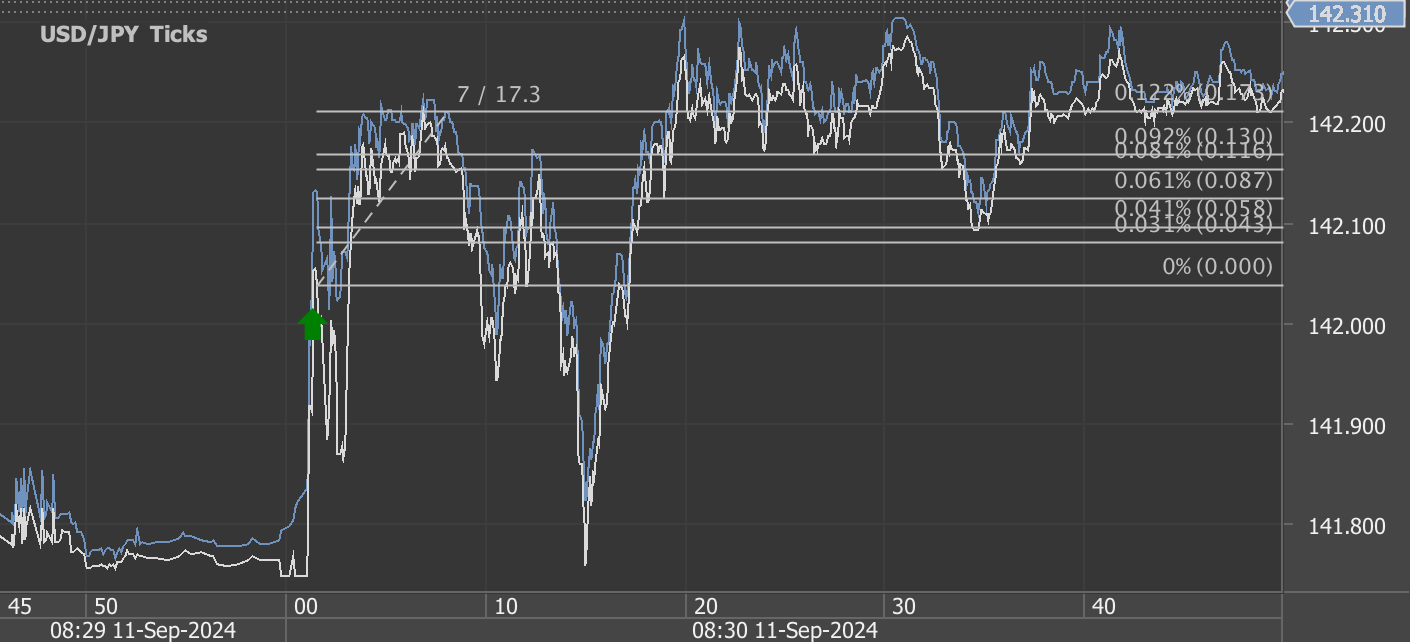

US BLS Consumer Price Index (CPI) (27 pips / 11 September 2024)

FOMC Interest Rate Decision and Projections (62 pips / 18 September 2024)

Total trading time would have been around 3 minutes! (preparation time not included)

September 2024 Economic Recap: Labor, Inflation, and the Fed's First Rate Cut

September 2024 saw a series of pivotal economic data releases and a significant policy shift from the Federal Reserve that sent ripples through markets. Three key events—Job Openings and Labor Turnover Survey (JOLTS), the Consumer Price Index (CPI), and the Federal Open Market Committee (FOMC) Interest Rate Decision—shed light on the current state of the U.S. economy, labor market, inflation, and monetary policy.

1. JOLTS Report – 4 September 2024

The JOLTS report for August revealed that job openings climbed to 8.04 million, reflecting a still-tight labor market. Despite economic uncertainties and ongoing monetary tightening, labor demand remains robust. This rise in job openings, from 7.7 million in July, suggests employers are continuing to hire, although higher wages might be contributing to persistent inflationary pressures. The tight labor market complicates the Federal Reserve's task of reducing inflation, as wage growth can fuel further price increases. The report's strong labor demand triggered a notable 72-pip movement in the market, signaling investor concerns about prolonged inflation and the Fed's response.

2. CPI Report – 11 September 2024

Inflation remained a focal point in September. The CPI data for August showed that inflation ticked up to 3.7% year-over-year, with core inflation (excluding food and energy) coming in at 4.2%. Energy prices, particularly gasoline, played a significant role in driving the overall increase, but inflation in housing and services continued to persist. This month-over-month rise of 0.2% matched July's figure and reinforced the idea that inflation remains sticky. Although the CPI report didn’t cause significant market turmoil (just a 27-pip reaction), it confirmed that the inflationary landscape still warrants the Federal Reserve’s attention.

3. FOMC Interest Rate Decision – 18 September 2024

In the most significant economic move of the month, the FOMC announced a 50 basis point rate cut, lowering the federal funds rate to a range of 4.75% - 5.00%. This marked the first rate cut since the Federal Reserve's aggressive tightening campaign began in 2022 to combat high inflation. Despite the cut, the central bank signaled a cautious stance, indicating that it would not rush into further cuts unless inflation showed clearer signs of easing toward the Fed’s 2% target. This decision was a response to slower economic growth and modest improvements in inflation but also acknowledged the risks of premature policy easing. The cut triggered a 62-pip reaction, as investors recalibrated their expectations for future rate cuts, with some projecting more reductions in the coming months.

What’s Next?

The combination of a resilient labor market, persistent inflation, and the Federal Reserve’s cautious but responsive policy shift signals a period of continued uncertainty. The Fed’s next steps will heavily depend on how inflation evolves in the coming months. The JOLTS data suggests that labor market tightness will continue to drive wage growth, potentially making it harder to rein in inflation. The CPI report shows that while inflation is slowing, it’s still not at the level the Fed desires. The rate cut may provide some relief to borrowers, but the Fed remains committed to its dual mandate of full employment and price stability.

Investors and market participants will closely watch upcoming data, particularly for signs of labor market softening and further inflation moderation, which will influence the Fed’s monetary policy trajectory into 2025.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Start futures/forex/oil/grains news trading with Haawks G4A low latency machine-readable data today, we offer one of the fastest machine-readable data feeds for US macro-economic and commodity data and macro-economic data from Norway, Sweden, Turkey, Switzerland and ECB interest rates and statement.

Please let us know your feedback and check out our G4A low latency data feed.

All data is machine readable and available via API access in Aurora, CH1, NY4 and LD4. Free trials.