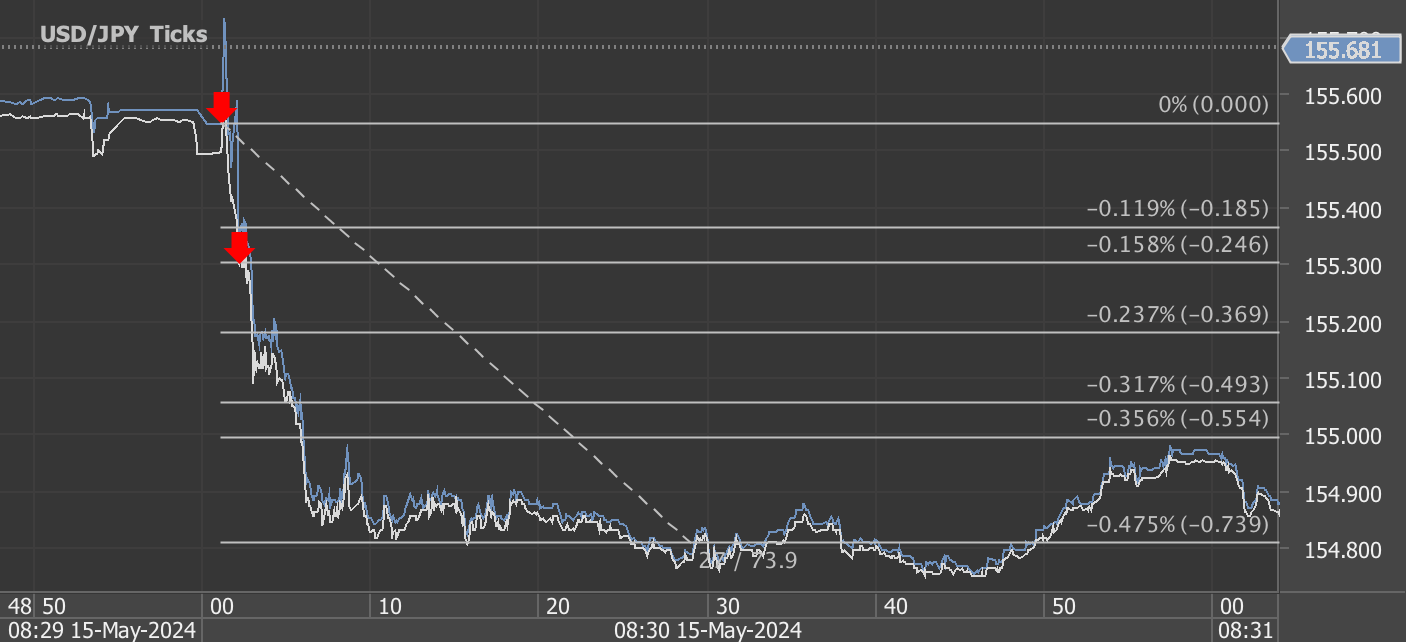

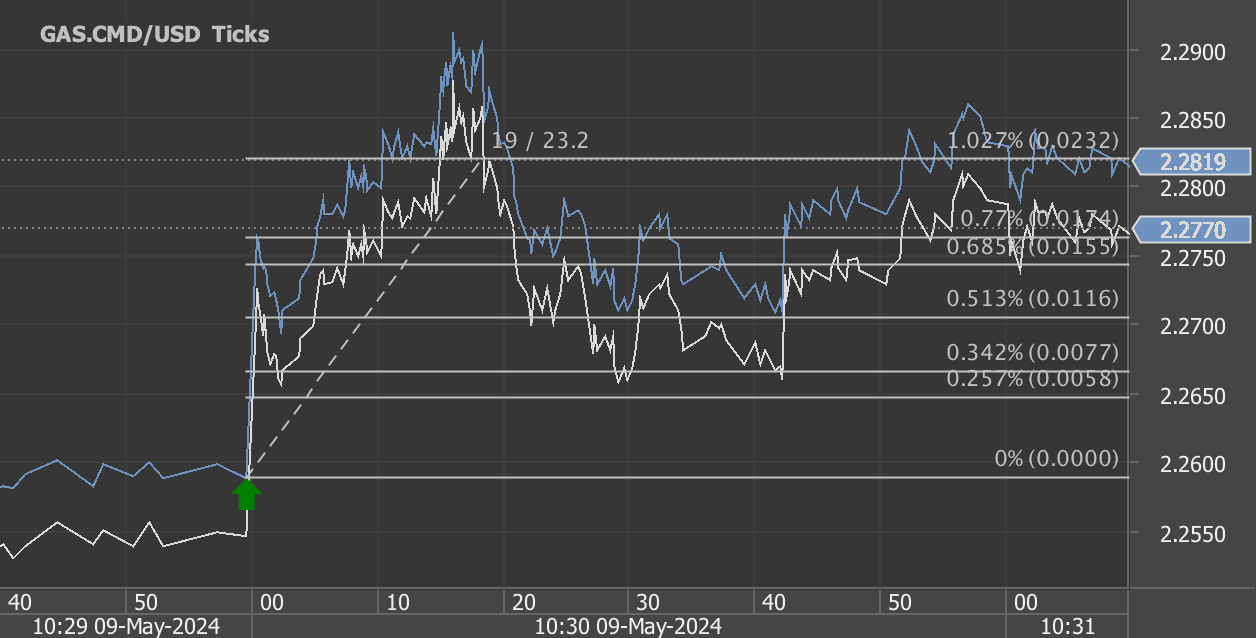

According to our analysis crude oil moved 33 ticks on DOE Petroleum Status Report data on 15 May 2024.

Light sweet crude oil (17 ticks)

Brent crude oil (16 ticks)

Charts are exported from JForex (Dukascopy).

Analyzing the Latest Trends in U.S. Petroleum Data as of May 2024

The latest Weekly Petroleum Status Report from the U.S. Energy Information Administration provides key insights into the petroleum market for the week ending May 10, 2024. As energy markets fluctuate, this data is crucial for understanding the current state of supply, demand, and pricing within the sector.

Refinery Inputs and Capacity Utilization

U.S. crude oil refinery inputs showed a significant increase, averaging 16.3 million barrels per day, up by 307,000 barrels from the previous week. This indicates a robust demand for refining capacity, which operated at an impressive 90.4% of its total available capacity. This high utilization rate suggests that refineries are ramping up operations possibly in response to anticipated demand or attractive margins on refined products.

Production Increases

Both gasoline and distillate fuel production saw increases last week. Gasoline production rose to an average of 9.7 million barrels per day, while distillate fuel production, which includes diesel and heating oil, also increased to 4.8 million barrels per day. These increases are indicative of refineries adjusting outputs to meet shifting market demands or to replenish inventories.

Import and Inventory Shifts

Interestingly, U.S. crude oil imports averaged 6.7 million barrels per day last week, marking a decrease of 226,000 barrels per day compared to the previous week. Over the last four weeks, however, imports have shown an overall increase of 7.1% compared to the same period last year. This rise could be attributed to various factors including pricing arbitrage opportunities or efforts to bolster reserves.

U.S. commercial crude oil inventories decreased by 2.5 million barrels, underscoring a drawdown that positions current stocks about 4% below the five-year average for this time of year. This reduction in crude inventories could be a sign of stronger demand or a strategic inventory management by market participants.

Fuel Stock and Prices

While total motor gasoline inventories slightly declined, distillate fuel inventories experienced a slight decrease, staying about 7% below the five-year average. This lower inventory level for distillates might signal tightness in the diesel market, possibly leading to higher future prices if the trend continues.

Propane/propylene inventories increased by 2.9 million barrels and are notably 14% above the five-year average. This could be due to lower demand or increased production, leading to higher stocks.

Price Movements

The price for West Texas Intermediate crude settled at $79.81 per barrel, marking a modest increase from the previous week and a significant rise compared to last year. Retail gasoline prices have seen a decline from last week, although they remain slightly higher than the previous year's figures. This could reflect the recent changes in crude prices and refinery outputs.

Conclusion

The data from the week ending May 10, 2024, highlights several important trends in the U.S. petroleum market. Increased refinery output and capacity utilization coupled with fluctuating imports and inventories suggest a dynamic market adjusting to both domestic and international pressures. Prices are reflecting these shifts, with notable implications for consumers and businesses alike. As the market continues to evolve, it will be important to monitor these trends for a deeper understanding of the broader economic landscape influenced by energy commodities.

Source: https://www.eia.gov/petroleum/supply/weekly/pdf/highlights.pdf

Start futures forex fx crude oil news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE Petroleum Status Report data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.