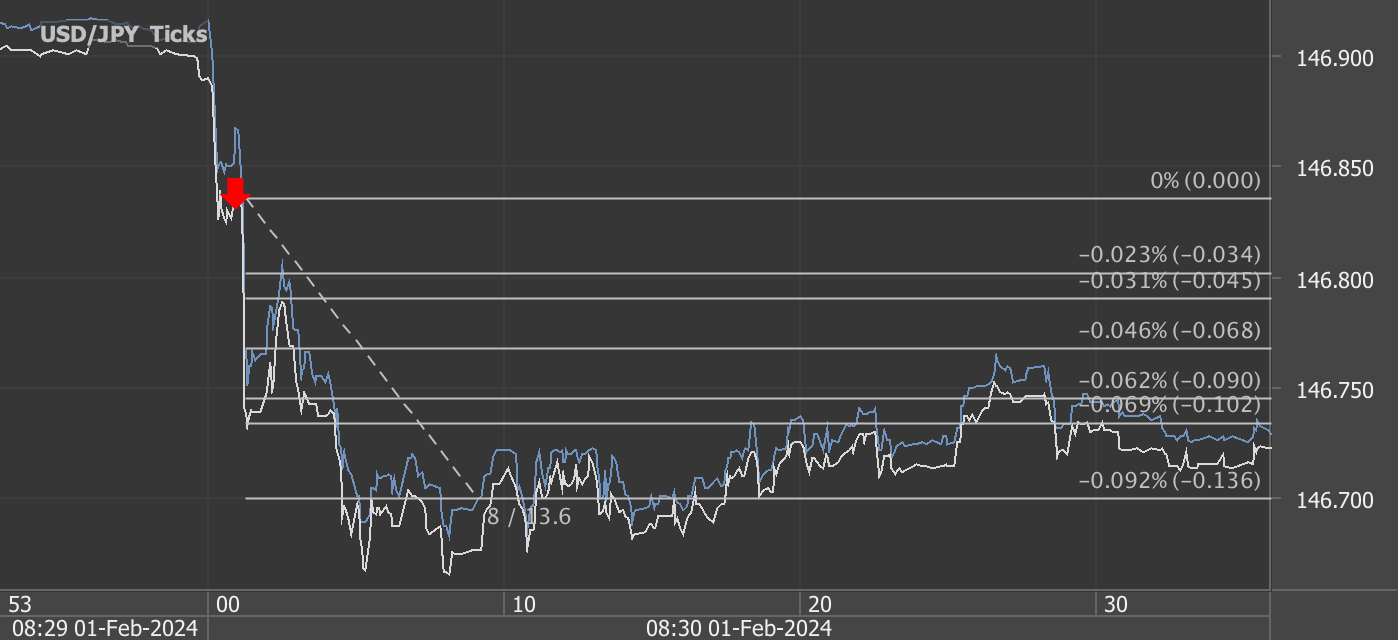

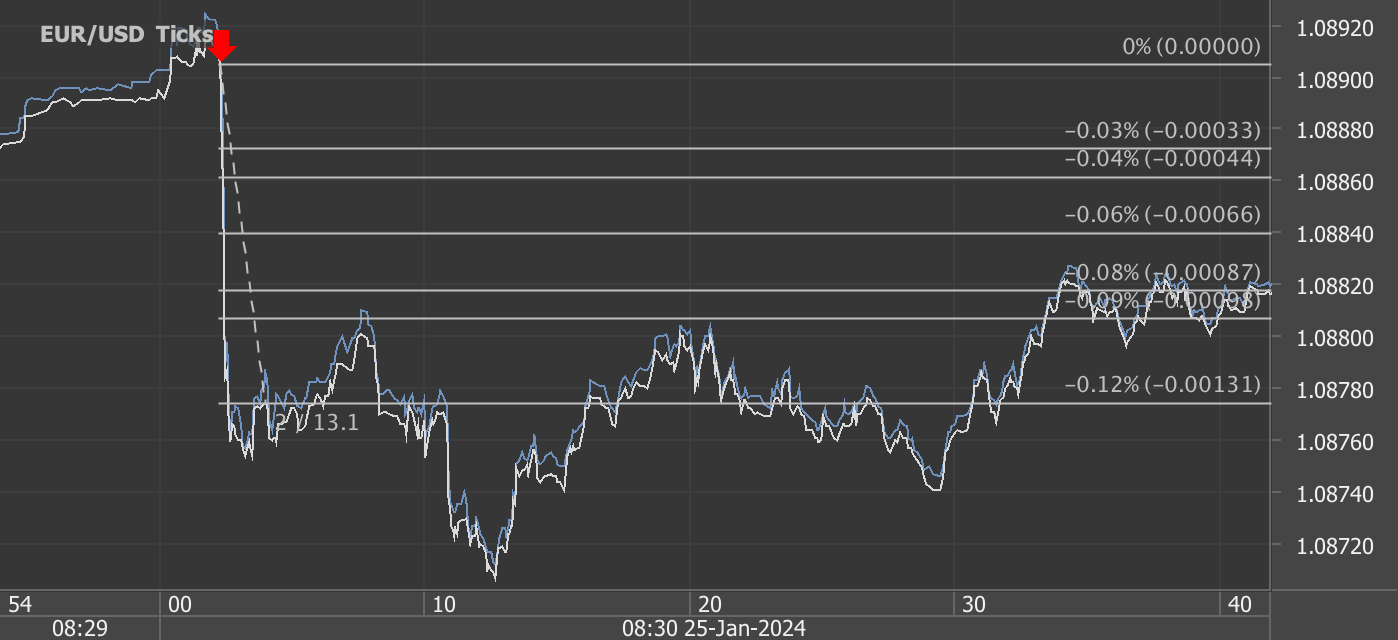

According to our analysis USDJPY and EURUSD moved 35 pips on US Philadelphia Federal Reserve Bank Manufacturing Business Outlook Survey data and US Retail Sales data on 15 February 2024.

USDJPY (21 pips)

EURUSD (14 pips)

Charts are exported from JForex (Dukascopy).

Analyzing the Latest Economic Indicators: Retail Sales and Manufacturing Sector Insights

In the ever-evolving landscape of the U.S. economy, recent releases from the Commerce Department and the Federal Reserve Bank offer critical insights into consumer behavior and manufacturing activity. The Advance Monthly Sales for Retail and Food Services report and the February 2024 Manufacturing Business Outlook Survey provide a mixed picture of the current economic environment, with signs of resilience in certain sectors despite overarching challenges. Let's delve into the details of both releases to understand their implications.

Retail Sales Take a Slight Dip with a Silver Lining

According to the Commerce Department's report for January 2024, U.S. retail and food services sales saw a minor retreat, marking a 0.8 percent decrease from the previous month, yet they experienced a 0.6 percent increase from January 2023. This nuanced performance underscores a broader trend of cautious consumer spending amidst economic uncertainties. Total sales for the November 2023 through January 2024 period, however, were up 3.1 percent from the same period a year ago, indicating a sustained appetite for retail and food services over the longer term.

The report also highlighted significant sectoral disparities. While traditional retail trade sales dipped slightly, nonstore retailers and food services continued to exhibit strong growth, suggesting a shift in consumer preferences towards online shopping and dining out. This divergence reflects the dynamic nature of consumer spending patterns and the ongoing adaptation of the retail sector to changing tastes and technological advancements.

Manufacturing Sector Shows Signs of Cautious Optimism

The Federal Reserve Bank's February 2024 Manufacturing Business Outlook Survey presents a cautiously optimistic view of the manufacturing sector. After months of subdued activity, the survey's indicators for general activity and shipments turned positive, signaling a potential rebound. However, the new orders index, despite improvements, remained in negative territory, indicating persistent challenges in demand.

Employment in the manufacturing sector appears to be contracting, with the employment index dropping to its lowest reading since May 2020. This suggests that manufacturers are becoming more cautious in their hiring, possibly due to uncertainties about future demand and operational costs.

Price indexes, while indicating overall increases, remain below long-run averages, hinting at a complex pricing environment where firms are possibly facing pressures to manage costs amidst fluctuating demand.

Looking ahead, the survey's future activity indicators suggest that manufacturers are growing more optimistic about growth over the next six months. This optimism is reflected in the expectations for increased activity, new orders, and even capital expenditures, pointing towards a cautious but hopeful outlook for the manufacturing sector.

Conclusion

The contrasting narratives from the retail and manufacturing sectors highlight the multifaceted nature of the current economic landscape. On one hand, consumer spending in the retail sector shows resilience, with significant growth in online shopping and food services. On the other hand, the manufacturing sector, while facing immediate challenges, is cautiously optimistic about the future.

These developments suggest that while the economy navigates through uncertainties, certain sectors continue to adapt and find growth opportunities. For businesses and policymakers, understanding these nuanced dynamics is crucial for making informed decisions and fostering a supportive environment for growth and stability in the changing economic climate.

Source: https://www.census.gov/retail/sales.html, https://www.philadelphiafed.org/surveys-and-data/regional-economic-analysis/mbos-2024-02

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.

Start futures forex fx news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.