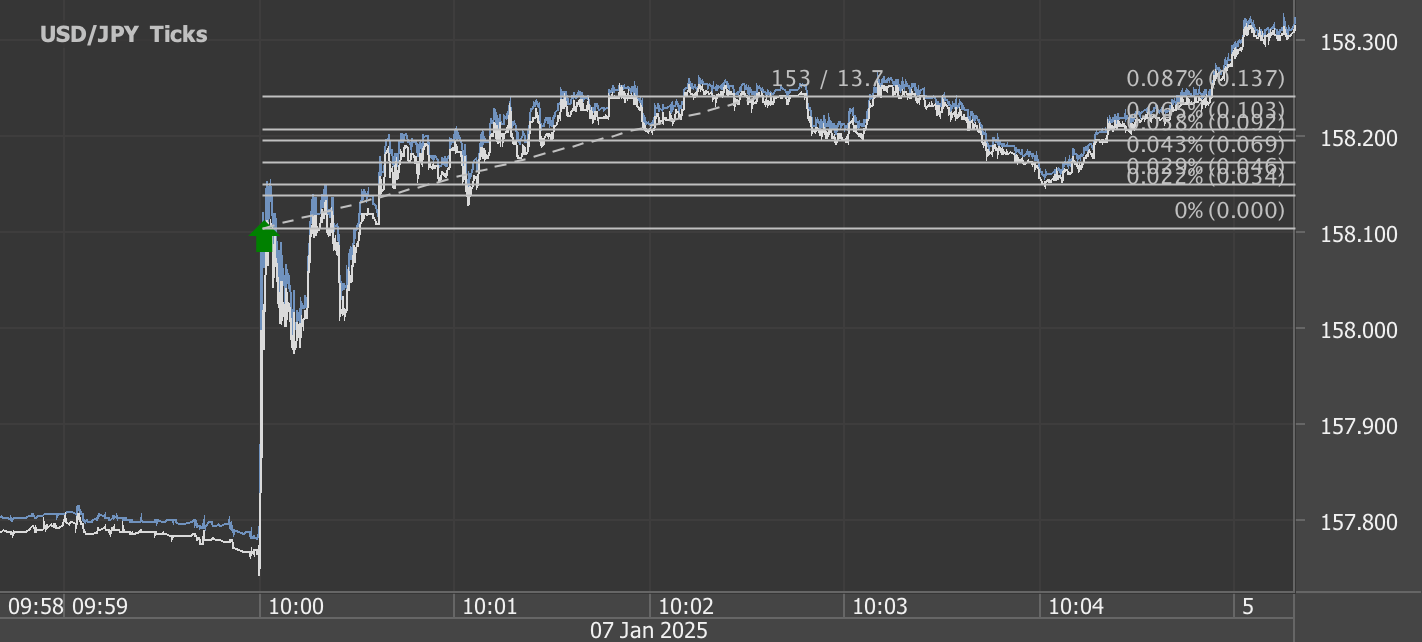

According to our analysis USDJPY and BTC moved 20 pips and 280 points on US Retail Sales data on 14 February 2025.

USDJPY (20 pips)

BTC (280 points)

Charts are exported from JForex (Dukascopy).

Market Reaction: USD/JPY Drops, Bitcoin Rallies After Weak Retail Sales Data

📅 February 14, 2025

The latest U.S. retail sales report has sent ripples through financial markets, causing USD/JPY to drop 20 pips while Bitcoin surged 280 points. With traders reacting swiftly to the data, let’s break down what’s happening and how you can capitalize on the volatility.

📉 USD/JPY Falls 20 Pips – Weak U.S. Data Weighs on Dollar

The U.S. retail and food services sales for January fell 0.9% from December, worse than market expectations. While still up 4.2% YoY, the weaker month-over-month figure has sparked concerns about consumer spending trends.

💡 Market Reaction:

The dollar weakened as traders reassess Fed rate cut expectations—a slowdown in retail activity could push the Fed to ease sooner.

USD/JPY fell 20 pips as demand for the safe-haven yen increased.

U.S. Treasury yields ticked lower, signaling growing expectations of monetary easing.

🚀 Bitcoin Rallies 280 Points – Risk-On Sentiment Creeping Back?

Bitcoin surged 280 points following the report, as traders bet on softer economic data fueling rate cut speculation. With lower rates favoring risk assets, BTC has resumed its upward momentum.

📢 Final Thoughts

Today’s retail sales report has triggered FX and crypto volatility, with USD/JPY sliding and Bitcoin soaring. As traders digest the data, all eyes will be on Fed policy signals and risk sentiment in the coming days.

🚀 What’s your move? Are you shorting USD/JPY or riding the BTC rally? Drop your strategy in the comments!

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.

Start futures forex fx news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.